Making Best Use Of the Benefits of Home Loans: A Step-by-Step Strategy to Safeguarding Your Perfect Residential Or Commercial Property

Navigating the facility landscape of home loans needs a systematic technique to make sure that you protect the home that lines up with your monetary objectives. To absolutely make best use of the advantages of home finances, one should consider what steps follow this fundamental work.

Understanding Mortgage Fundamentals

Understanding the principles of home mortgage is important for any individual taking into consideration buying a residential or commercial property. A home mortgage, often referred to as a home mortgage, is a financial product that permits individuals to obtain money to acquire property. The debtor accepts pay off the loan over a defined term, typically ranging from 15 to three decades, with interest.

Secret components of home mortgage include the principal quantity, rates of interest, and settlement routines. The principal is the amount obtained, while the passion is the expense of borrowing that amount, expressed as a percent. Rate of interest can be dealt with, remaining continuous throughout the funding term, or variable, varying based upon market problems.

Additionally, customers need to understand numerous kinds of home mortgage, such as conventional car loans, FHA car loans, and VA financings, each with unique eligibility standards and advantages. Understanding terms such as deposit, loan-to-value proportion, and private mortgage insurance policy (PMI) is likewise essential for making notified decisions. By grasping these basics, prospective home owners can navigate the intricacies of the home mortgage market and identify alternatives that line up with their monetary goals and home aspirations.

Evaluating Your Financial Circumstance

Assessing your economic situation is an essential step prior to starting the home-buying journey. This analysis includes an extensive evaluation of your income, expenses, cost savings, and existing financial debts. Begin by determining your total regular monthly income, consisting of incomes, incentives, and any kind of additional sources of earnings. Next off, listing all monthly costs, making sure to account for repaired expenses like rental fee, utilities, and variable expenditures such as grocery stores and enjoyment.

After developing your earnings and costs, determine your debt-to-income (DTI) ratio, which is necessary for lenders. This proportion is computed by separating your complete monthly financial debt payments by your gross monthly revenue. A DTI proportion listed below 36% is usually considered favorable, suggesting that you are not over-leveraged.

In addition, examine your credit report, as it plays a pivotal role in safeguarding beneficial funding terms. A higher credit report can bring about lower rate of interest, eventually conserving you cash over the life of the car loan.

Exploring Funding Choices

With a clear image of your monetary circumstance developed, the following step involves checking out the numerous lending alternatives available to possible property owners. Comprehending the different kinds of home mortgage is essential in choosing the ideal one for your demands.

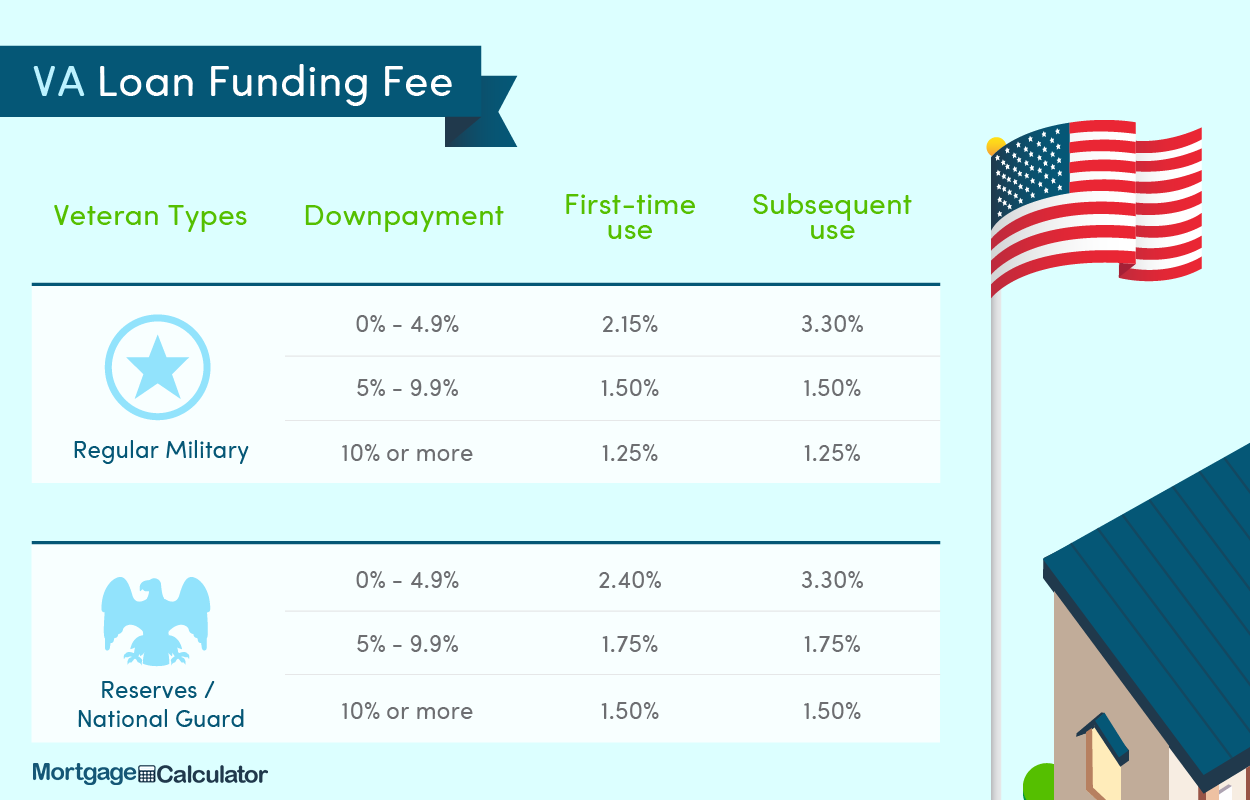

Standard lendings are typical financing techniques that generally require a greater credit rating and deposit however offer affordable rate of interest. Alternatively, government-backed loans, such as FHA, VA, and USDA lendings, cater to specific groups and commonly need lower deposits and credit ratings, making them easily accessible for first-time buyers or those with restricted funds.

One more alternative is adjustable-rate home mortgages (ARMs), which feature lower initial prices that change after a specific duration, possibly bring about considerable financial savings. Fixed-rate home mortgages, on the other hand, supply security with a regular rates of interest throughout the financing term, guarding you versus market fluctuations.

In addition, think about the loan term, which commonly ranges from 15 to 30 years. Shorter terms may have higher regular monthly settlements however can save you rate of interest gradually. By carefully examining these alternatives, you can make an informed choice that aligns with your economic objectives and homeownership desires.

Preparing for the Application

Successfully preparing for the application process is essential for safeguarding a mortgage. This phase prepares for getting favorable funding terms and makes sure a smoother authorization experience. Begin by analyzing your monetary circumstance, which consists of assessing your credit rating, earnings, and existing financial debt. A strong credit history is crucial, as it affects the loan quantity and rates of interest readily available to you.

Organizing these files in advancement can considerably speed up the application process. This not only provides a clear understanding of your borrowing ability yet additionally reinforces your setting when making a deal on a property.

Additionally, identify your spending plan by factoring in not just the car loan amount but additionally home taxes, insurance, and upkeep prices. Ultimately, familiarize on your own with numerous lending types and their corresponding terms, as this knowledge will equip you to make educated decisions throughout the application procedure. By taking these positive actions, you will certainly enhance your readiness and increase your possibilities of protecting the mortgage that ideal fits your requirements.

Closing the Bargain

:max_bytes(150000):strip_icc()/va-home-loans-1798389_FINALv2-d42807494ecd4966aed01de64838b89c.png)

Throughout the closing meeting, you will review and authorize various documents, such as the car loan estimate, shutting disclosure, and home mortgage contract. It is crucial to extensively recognize these files, as they detail the finance terms, payment timetable, and closing costs. Take the time to ask your lender or realty agent any questions you may have to avoid misconceptions.

When all files are signed and funds are transferred, you will receive the keys to your new home. Bear in mind, shutting costs can differ, so be gotten ready for expenses that may include evaluation costs, title insurance, and attorney charges - VA Home Loans. By remaining arranged and notified throughout this process, you can guarantee a smooth shift into homeownership, optimizing the advantages of your home mortgage

Final Thought

In final thought, making best use of the benefits of mortgage requires a methodical technique, incorporating a complete assessment of financial circumstances, expedition of varied finance options, and careful prep work for the application procedure. By adhering to these steps, prospective property owners can enhance their opportunities of safeguarding positive financing webpage and attaining their property ownership goals. Eventually, mindful navigating of the closing process better solidifies an effective shift right into homeownership, making certain lasting economic security and complete satisfaction.

Navigating the facility landscape of home finances needs a systematic technique to ensure that you protect the residential property that straightens with your monetary objectives.Recognizing the basics of home car loans is vital for any person use this link taking into consideration acquiring a residential property - VA Home Loans. A home funding, usually referred to as a home loan, is an economic item that permits individuals to borrow cash to get genuine estate.In addition, consumers should be conscious of different types of home finances, such as conventional lendings, FHA fundings, and VA fundings, each with distinct eligibility requirements and benefits.In conclusion, maximizing the advantages of home lendings demands an organized strategy, encompassing a comprehensive assessment of monetary circumstances, exploration of varied car loan alternatives, and thorough prep work for the application internet procedure